One of the most compelling reasons to live and work in the United Arab Emirates is the opportunity to earn a tax-free income. It is a massive financial advantage, but many residents let that hard-earned money sit idle in a basic current account, slowly losing value to inflation.

To truly optimize your financial future, you need to make your money work as hard as you do. The first step is choosing the right vehicle to grow your cash wealth. Whether you are a new expat just landing in Dubai, a long-term resident looking for better returns, or an entrepreneur who has just finished their business setup – perhaps with help from specialists like Emifast – getting your personal savings sorted is crucial.

This guide will cut through the noise, helping you compare options, understand the landscape, and find the best savings accounts in UAE to start maximizing your returns today.

Understanding the UAE Savings Landscape

Before comparing rates, it is important to understand the unique features of the UAE banking market.

Conventional vs. Sharia-Compliant Accounts

You will see two main types of banks: conventional and Islamic.

- Conventional Banks offer standard savings accounts that pay you a pre-determined interest rate.

- Islamic Banks operate according to Sharia principles, which forbid charging or paying interest. Instead, they invest your deposits in Sharia-compliant activities and share the resulting “profit” with you based on a pre-agreed ratio. For the saver, the outcome is similar – a return on your money – but the mechanism is different.

The Importance of Salary Transfer

Many banks in the UAE reserve their most attractive rates and benefits for customers who transfer their monthly salary to them. A “salary saver” account will often have a higher rate than a general savings account at the same bank.

Tiered Returns

It is common for savings accounts to have tiered rates. This means the interest or profit rate increases as your account balance grows. For example, you might earn 0.5% on the first AED 10,000, but 1.5% on balances above AED 50,000.

Key Features to Look for in a Top Savings Account

When evaluating the “best” account for your needs, look beyond just the headline rate. Consider these factors:

- High Annual Equivalent Rate (AER) or Profit Rate: Compare the annualized return you will receive.

- Low or No Minimum Balance: Some accounts charge a monthly fee (e.g., AED 25) if your balance drops below a certain limit (e.g., AED 3,000). Look for accounts that waive this.

- Robust Digital Banking: A top-tier mobile app for easy transfers, bill payments, and account management is essential.

- Multi-Currency Options: For expats, the ability to hold savings in USD, EUR, or GBP within the same bank can be highly valuable.

- Instant Access: Ensure you can withdraw your funds via ATM or transfer immediately without penalty if you need them for an emergency.

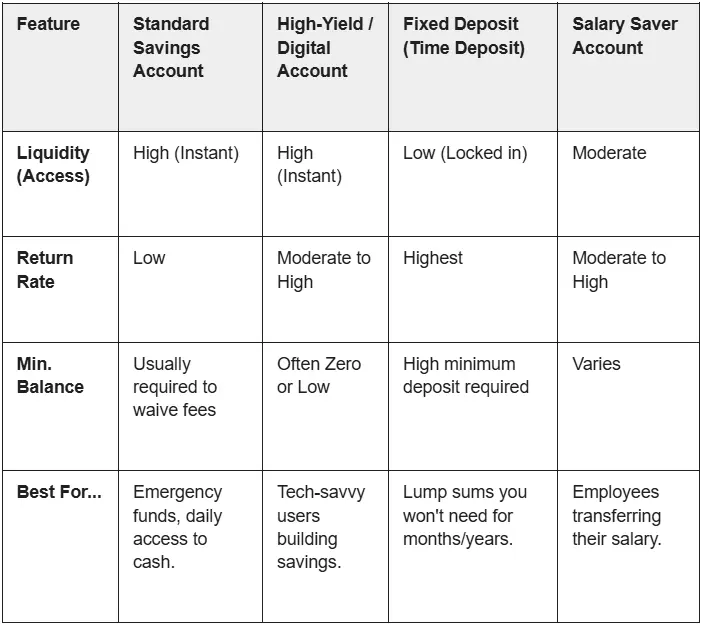

Comparative Snapshot: Types of Savings Accounts

This table breaks down the different categories of savings products available to help you choose the right fit.

How to Open a Savings Accounts in UAE

Thanks to digital innovations, opening an account has never been easier. Here is the typical process.

- Verify Your Eligibility: To open most accounts instantly, you must have a valid UAE residency visa and original Emirates ID.

- Gather Required Documents: Have your Emirates ID, Passport with residence visa page, and proof of income (like a salary certificate) ready.

- Choose Your Bank & Account: Based on your research, decide which bank and specific savings product suits you best.

- Apply via App (Recommended): Download the bank’s app. Most modern banks allow you to open an account in minutes using your UAE Pass for instant digital verification, without visiting a branch.

- Fund the Account: Make your initial deposit via bank transfer or cash deposit machine to activate the account and start earning returns immediately.

Need help choosing between banks or a digital solution? Our advisors are ready to assist you in navigating the evolving landscape of banking in the UAE.

Benefits of Optimizing Your UAE Savings Strategy

Taking the time to select the right account isn’t just about earning a few extra Dirhams; it’s a strategic financial move.

- Maximize Tax-Free Growth: You are already in a zero personal income tax environment. Use a high-yield account to capitalize on this and grow your wealth faster.

- Build a robust Emergency Fund: A dedicated, accessible savings account is the perfect place to keep 3-6 months of expenses in AED for peace of mind.

- Compound Your Wealth: The power of compounding means the interest or profit you earn will generate its own returns over time, accelerating your savings growth.

Conclusion: Start Growing Your Tax-Free Wealth Today

Your time in the UAE is a one-of-a-kind opportunity to create a solid financial future. Please don’t let your money sit idle. Just by spending a short time comparing your options and opening a high-yield savings account, you can make sure that your tax-free income is helping you reach your future goals.

Evaluate your choices, set up the appropriate account, and begin maximizing your wealth in the UAE right away.

Frequently Asked Questions About UAE Savings

Can expats open savings accounts in the UAE?

Yes, definitely. Expatriates holding a valid residency visa in the UAE and an Emirates ID are quite capable of opening savings accounts without any hassles. There are a handful of banks that provide ‘non-resident’ accounts; however, these usually come with a condition of maintaining a markedly high minimum balance and the account needs to be opened physically at the branch.

What is a good interest rate for savings in UAE?

Rates fluctuate based on central bank policies and market conditions. Currently, standard savings accounts offer very low rates. However, high-yield digital accounts, promotional salary accounts, or longer-term fixed deposits can offer significantly higher returns, sometimes exceeding 4-5% per annum depending on the term.

Is my money safe in UAE banks?

Yes. The UAE banking system is robust, stable, and highly regulated by the Central Bank of the UAE, ensuring a high degree of safety for depositors’ funds.

What is the difference between profit rate and interest rate?

A conventional bank pays you “interest.” An Islamic bank, which cannot deal in interest due to Sharia compliance, invests your money and pays you a share of the generated “profit.” Both are ways you earn a return on your savings.

Are there minimum balance fees?

Yes, many traditional savings accounts will charge a monthly fee if your average balance falls below a certain limit. However, a new wave of digital-first bank accounts has emerged that offer zero minimum balance requirements.