Understanding the UAE Banking Landscape

The UAE is a global financial hub with a robust regulatory framework governed by the Central Bank of the UAE (CBUAE). In 2026, the system has become highly digitized, integrating features like UAE PASS for instant identity verification, making the process faster than ever for residents.

Account Types

- Current Accounts: Designed for daily transactions. These come with a chequebook (essential for rent in the UAE) and a debit card. Usually requires a minimum salary or balance.

- Savings Accounts: Ideal for wealth preservation. Savings Accounts offer interest but often do not provide a chequebook.

- Non-Resident Accounts: Limited to savings/investment. Non-residents cannot typically access credit facilities or chequebooks.

- Corporate Accounts: Essential for businesses registered in the UAE (Mainland, Free Zone, or Offshore).

Eligibility and Document Checklist

The “Know Your Customer” (KYC) requirements in the UAE are strict. Having your documents pre-validated is the most important step.

For Residents (Personal)

To open a full-service account, you must have a valid residency visa.

- Passport: Original and copy (must be valid for at least 6 months).

- Emirates ID: The physical card (or digital version via the UAE PASS app).

- Proof of Residency: A registered tenancy contract (Ejari) or a recent utility bill (DEWA/SEWA).

- Proof of Income: A salary certificate from your employer or a valid labor contract.

- Bank Statements: Usually 3–6 months of statements from your previous bank (local or international).

For Non-Residents (Personal)

- Passport with entry stamp.

- Proof of Address from your home country (utility bill/bank statement).

- Reference Letter from your primary bank in your home country.

- Source of Wealth: Documentation explaining the origin of your funds.

For Corporate Entities

- Trade License: Valid UAE business license.

- MOA/AOA: Memorandum and Articles of Association.

- Shareholder Documents: Passports, Visas, and Emirates IDs of all UBOs (Ultimate Beneficial Owners).

- Business Plan: A brief overview of activities, expected turnover, and key suppliers/customers.

- Office Lease: Proof of physical presence (Mainland Ejari or Free Zone office certificate).

The Step-by-Step Process

In 2026, many banks will offer “Instant Account Opening” via mobile apps for residents. However, corporate and non-resident accounts still require a more manual touch.

- Select Your Bank: Choose based on your specific needs (e.g., high-volume trading vs. low minimum balance).

- Initial Application: Use the bank’s mobile app (for residents) or visit a branch.

- Digital Verification: If using an app, you will scan your Emirates ID and perform a “liveness check” (facial recognition).

- Compliance Review: The bank’s KYC department reviews your source of funds and business activity (for corporate).

- Account Activation: Once approved, you will receive your IBAN. You must then deposit the Initial Minimum Balance.

- Card/Chequebook Delivery: Usually delivered via courier within 2–3 business days.

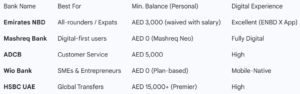

Top Banks in the UAE (2026 Comparison)

Key Financial Considerations

Minimum Balance Fees: Most banks charge a fee (typically AED 25–50) if your balance falls below the required threshold.

Account Currencies: Most banks offer multi-currency accounts (AED, USD, EUR, GBP).

Remittances: Look for banks with “DirectRemit” features to avoid high wire transfer fees when sending money home.

VAT: A 5% VAT is applicable to most banking services and administrative fees.

Challenges and Tips for Success

Pro Tip: If you are a business owner, avoid choosing a bank solely based on its “brand.” Some smaller banks are more welcoming to specific industries (like E-commerce or Consulting) than the “Big Three.”

- Be Patient: While personal accounts for residents can open in minutes, corporate accounts for high-risk industries (like Crypto, Gold, or Real Estate) can take 4–8 weeks.

- Maintain a Physical Office: Banks in 2026 still prioritize companies with a “real” presence. Using a virtual desk can sometimes lead to account rejection.

- Transparent Sourcing: If you are depositing a large sum immediately, have the “Source of Wealth” documents (sales contracts, inheritance, or investment dividends) ready.

Frequently Asked Questions (FAQs)

- Can I open a UAE bank account from abroad?

Generally, no. Most banks require a physical presence for an “in-person” signature or a digital liveness check using the UAE PASS app, which requires you to be in the country. However, some international banks may allow initial paperwork to start remotely if you have a “Priority” or “Private Banking” relationship.

- How long does it take to open a corporate bank account?

While personal accounts for residents can often be opened instantly via an app, corporate accounts are subject to rigorous compliance checks. In 2026, the average timeline is:

- Digital Banks (e.g., Wio): 3 to 10 working days.

- Traditional Banks: 4 to 8 weeks, depending on the complexity of the business activity.

- Is it possible for a non-resident to get a chequebook?

No. In the UAE, chequebooks are strictly reserved for residents with a valid residency visa. Non-residents are typically restricted to savings accounts and do not have access to credit facilities or chequebooks.

- Why was my bank account application rejected?

Rejections are usually due to “Compliance” or “Internal Policy.” Common reasons include:

- High-risk business activity (e.g., unregulated crypto, gold trading, or certain high-risk jurisdictions).

- Inability to prove “Source of Wealth” or “Source of Funds.”

- Lack of a physical office (virtual offices are often scrutinized heavily).

Inconsistent bank statements from your home country.